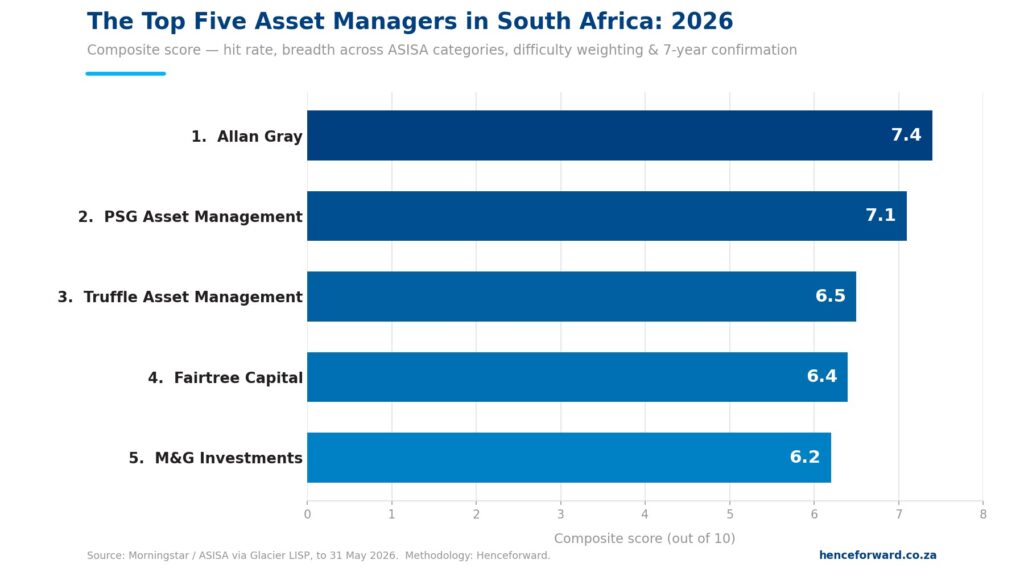

On five-year performance data to the end of May 2026, the five strongest active asset managers in South Africa are Allan Gray, PSG Asset Management, Truffle Asset Management, Fairtree Capital, and M&G Investments. The ranking is built on a composite of how consistently each manager’s funds beat their peers, across how many categories they do it, and whether those results hold up over a longer seven-year window.

Deciding who the best asset managers in South Africa are will always involve some subjectivity. But when you sit with data covering more than 1,400 qualifying retail funds across 14 ASISA categories, patterns emerge that are hard to argue with. This year’s rankings update last year’s analysis and refine the methodology behind it.

Some familiar names are back near the top after years in the shadows. Others that were dominant recently have slipped. A couple of long-standing favourites are in territory that would have been hard to predict two years ago. The data tells a story worth understanding — not just for the rankings themselves, but for what it reveals about how active management actually works over a full market cycle. For the broader framework these managers sit within, our investment guide and offshore investing guide are a useful starting point.

Key Definitions

Asset management

The professional management of collective investment funds — unit trusts, ETFs, and similar structures — on behalf of investors. In South Africa these funds fall under ASISA categories such as Multi-Asset High Equity, SA Equity General, or Income, which group funds with similar mandates for fair peer comparison.

Top quartile (Q1)

A fund ranked in the top 25% of its ASISA peer group over a given period. It is the industry-standard measure of outperformance and the basis on which most DFMs and investment committees assess manager skill.

Top decile (D1)

A fund ranked in the top 10% of its peer group — a more demanding standard introduced in our 2026 methodology that distinguishes genuinely elite performance from solid-but-not-exceptional results.

Seven-year confirmation

Whether a fund that ranks top quartile over five years also ranks top quartile over seven. A fund that achieves both is far more likely to be a product of skill than one that only shows over the shorter window.

White-label attribution

Our practice of assigning sub-advised funds to the actual investment manager, not the brand on the label. Truffle, for example, sub-advises the Amplify SCI Wealth Protector Fund — so that fund is attributed to Truffle in our analysis.

How We Rank Asset Managers: Evolving the Methodology

Last year we ran this analysis using seven-year returns as the primary screen. It was a reasonable starting point, but it has a blind spot: it excludes newer managers with shorter track records and can reward managers who had a strong run a decade ago but have since slipped. For 2026, we shifted the primary lens to five-year returns, while using seven-year performance as a confirmation filter. The logic is straightforward — five years captures a meaningful market cycle, including the post-COVID recovery, the inflation shock, and the subsequent value rotation. Seven years adds historical context. Together they give a cleaner picture of current form without sacrificing long-term rigour.

We also introduced a tiered scoring system this year. Rather than treating all top-quartile funds equally, we now distinguish between funds in the top decile (D1, the top 10%) and those in the top quartile but outside the top decile. Top-decile performance earns three times the weight in our hit-rate calculation. This separates managers who are genuinely elite — producing multiple funds with the very best returns in large peer groups — from those who are consistently above average but rarely exceptional.

The three scoring components remain broadly the same: hit rate (40%), breadth across categories (35%), and a difficulty weighting based on peer group size (25%). We also apply a seven-year confirmation bonus: managers whose top-quartile five-year funds also confirm over seven years earn a meaningful uplift. Fund-of-fund products, money market funds, and pure DFM platforms are excluded. Where a manager sub-advises under another brand, we attribute the fund to the actual investment manager.

| Scoring Component | Weight | What it measures |

|---|---|---|

| Hit rate (tiered D1/Q1) | 40% | Share of a manager’s funds in the top quartile, with top-decile funds weighted 3× |

| Breadth across ASISA categories | 35% | Number of distinct categories where the manager has a top-quartile fund |

| Difficulty weighting | 25% | Log-scaled by peer group size — winning in a 189-fund category scores higher than winning in a 34-fund one |

| 7Y confirmation bonus | Additive | Top-quartile five-year funds that also confirm over seven years earn a score uplift |

The data covers retail funds available on major South African platforms, screened across 14 ASISA categories with at least 15 peer funds, as at 31 May 2026. Where a manager has multiple share classes of the same fund, we use the primary retail class (typically A1 or A). Rankings reflect performance in context — not just raw returns, but how those returns compare within the right peer group.

The Top Five Asset Managers in South Africa: 2026

Below is a summary of the composite scores for our top five active managers, followed by the narrative behind each ranking.

| Rank | Manager | Qualifying Funds | Top Decile (D1) | Top Quartile (Q1) | 7Y Confirmed | Categories | Score |

|---|---|---|---|---|---|---|---|

| 1 | Allan Gray | 7 | 3 | 5 | 4/5 | 4 | 7.4 |

| 2 | PSG Asset Management | 18 | 6 | 7 | 7/7 | 7 | 7.1 |

| 3 | Truffle Asset Management | 5 | 2 | 4 | 4/4 | 3 | 6.5 |

| 4 | Fairtree Capital | 10 | 1 | 5 | 4/5 | 5 | 6.4 |

| 5 | M&G Investments | 8 | 0 | 5 | 1/5 | 5 | 6.2 |

Based on Morningstar/ASISA performance data to 31 May 2026. Fund-of-fund products excluded. White-label funds attributed to the actual investment manager. Passive managers assessed separately.

#1: Allan Gray — Back at the Top, and the Numbers Explain Why

Allan Gray has occupied more or less every position in industry rankings over the past decade. They were dominant for much of the 2000s and 2010s, then went through a prolonged period where their contrarian, value-oriented process was genuinely out of step with what global markets rewarded. Growth stocks surged; value lagged; patient managers got punished. Allan Gray didn’t change their process — they just waited.

The five years to May 2026 vindicated that patience. Their Balanced Fund delivered 13.9% per annum — placing it in the top decile of a 189-fund peer group and confirming the result on the seven-year number. The Orbis Global Equity Feeder, which gives clients access to Allan Gray’s offshore sibling’s stock-picking, returned 16.7% p.a. over five years — again top decile, again confirmed on seven years. The Stable Fund at 10.9% remains top quartile. Of the five Allan Gray funds that land in the top quartile, four confirm their five-year result on the seven-year track record. That combination — breadth, depth, and durability — is what puts them at the top of this year’s ranking.

It’s worth naming what this actually reflects. Allan Gray has always run a concentrated, high-conviction book. They own fewer stocks than most, hold them for longer, and are willing to be wrong for extended periods if the underlying thesis remains intact. That approach is uncomfortable in trending markets. But when the cycle turns — when the market starts pricing businesses on fundamentals rather than momentum — Allan Gray tends to look prescient. That is arguably what the past five years represent.

#2: PSG Asset Management — The Value Thesis, Delivered

If Allan Gray’s comeback is the story of patient conviction, PSG’s performance over this period is something more emphatic. PSG Equity returned 19.6% per annum over five years — the highest five-year return of any fund in our South African Equity General peer group. PSG Balanced returned 16.2%, placing it comfortably in the top decile of a 189-fund category. PSG Flexible came in at 17.1%, similarly top decile. The Global Equity feeder at 15.9% is also top decile in a competitive global peer group. Every one of those results confirms on the seven-year number.

PSG Asset Management runs a deep value philosophy with a contrarian overlay. For a long period — particularly during the 2016–2021 global growth rally — this approach was a significant headwind. Their funds underperformed, clients left, and the approach was widely questioned. The team stuck to the process. The market eventually came to them.

The breadth of PSG’s outperformance is striking. Their seven top-quartile funds span equities, balanced, income, global equity, and global flexible — seven distinct ASISA categories, the widest breadth of any manager in our analysis. Seven out of seven confirm on the seven-year horizon. On our composite scoring they sit just behind Allan Gray on points, but their top-decile count is actually higher — six D1 funds versus Allan Gray’s three. We give Allan Gray the edge at number one on the durability and consistency narrative, but PSG is very close, and in raw top-decile terms is arguably the standout manager of the past five years.

#3: Truffle Asset Management — The Quiet Achiever, Still

Truffle has appeared in our rankings consistently and there is a reason for that. They are not a large or widely known brand. They don’t run the biggest funds or spend on distribution. What they do is manage money with a disciplined, research-driven process and produce results that hold up over time. Every fund they placed in the top quartile over five years also confirms in the top quartile over seven. That is a perfect confirmation rate, and it is not common.

Truffle sub-advises mandates for Amplify, so their reach is broader than their own brand suggests. The Amplify SCI Wealth Protector Fund — one of the better-known conservative balanced options in the market — is a Truffle-managed product. Their own General Equity fund at 14.3% over five years sits comfortably in the top quartile of SA equities. Their Income Plus fund at 9.8% is top decile in a 37-fund peer group. The range is focused, not sprawling, and every fund in it is genuinely competitive.

Truffle’s drop from #2 in last year’s ranking to #3 this year is almost entirely a function of the methodology shift from a seven-year to a five-year primary horizon — their long-run record remains excellent — and the arrival of Allan Gray and PSG with particularly strong five-year numbers. On consistency and seven-year durability, Truffle is as good as anyone on this list.

#4: Fairtree Capital — Still Excellent, Tighter This Year

Fairtree was number one in last year’s ranking. Dropping to four will raise eyebrows, and it deserves an honest explanation. The short answer is that their flagship Balanced Fund returned 12.2% per annum over the five years to May 2026. That is a good return. The top-quartile cutoff in the 189-fund High Equity category is 12.31%. The difference between Fairtree Balanced being a top-quartile fund and a second-quartile one — this year — is 11 basis points. Eleven. On a seven-year basis, the same fund is clearly top quartile. The quality is intact.

What Fairtree’s fourth-placed position reflects is not a deterioration in their investment process. It reflects the way a single tighter five-year window lands on a single fund. Across the rest of their range — the Select Equity fund at 14.6%, the Global Equity feeder at 13.6%, the ALBI Plus fixed income fund at 12.5%, the BCI Income Plus at 9.4% — Fairtree is top quartile and confirms those results on seven years. Their breadth across five different ASISA categories is the widest of any manager in the top five. The Balanced Fund aside, this is a manager firing consistently across the board.

For advisers and investors, the practical implication is that Fairtree belongs on this list and their broader range continues to perform. The Balanced Fund remains a high-quality, well-run portfolio that has simply had a tighter five-year return profile than the category demanded. That is not a reason to dismiss the manager — it is a reason to read the data carefully rather than rankings in isolation.

#5: M&G Investments — Under the Radar, but Not for Much Longer

If you don’t recognise the name M&G Investments, you almost certainly recognise their previous identity. This is Prudential Investment Managers, which rebranded to M&G in South Africa in 2022. The team, the philosophy, and the process are the same — the label changed, not the capability.

M&G has had a quiet few years from a marketing standpoint, but the data tells a different story. Their Balanced Fund returned 12.3% over five years — top quartile in 189 funds. Their Inflation Plus fund at 11.2% is top quartile in low equity. Their Enhanced Income fund at 9.6% is top quartile in multi-asset income. Their Dividend Maximiser equity fund at 14.2% is top quartile in SA equities and also confirms on seven years. They have top-quartile funds across five distinct ASISA categories — among the widest breadth of any manager in the top ten.

The honest caveat on M&G is the seven-year confirmation number: only one of their five top-quartile funds confirms on the seven-year track record. This suggests their resurgence is relatively recent — probably the past three to four years — rather than sustained over a full decade. That weakens their case compared with Allan Gray or Truffle, and it is why they sit at five rather than higher. But as a value-tilted manager whose approach is coming back into fashion, the trajectory is worth noting. Their five-year result is real. The durability is the open question.

Why Some Familiar Names Are Not in the Top Five

Sygnia: Broad Consistency, but Diluted by Scale

Sygnia’s consistency record is impressive: six of six top-quartile funds on five years also confirm on seven years — a perfect confirmation rate. The problem is that they manage 17 qualifying funds and only two of them reach the top-decile threshold. The Skeleton balanced range produces solid top-quartile results across low, medium, and high equity mandates, but these are essentially index-linked products competing in peer groups that include active managers with higher returns. Sygnia FANG.AI, with a 22.3% five-year return, is genuinely exceptional — but one elite fund in a 17-fund range doesn’t produce the hit-rate profile our composite requires. Sygnia is an excellent manager of passive and systematic strategies; on our active-management framework, the dilution of quality across a large shelf limits their composite score. They sit at seven in the full ranking — not far off, and their consistency credentials are real.

Coronation: A Difficult Period That Demands Honesty

Coronation was, for much of the 2000s and 2010s, arguably the standard against which South African active management was measured. Their macro insights, deep research culture, and long-term orientation produced extraordinary long-run results. They remain a serious organisation with serious people.

The five-year numbers, however, are hard to defend. One of eleven qualifying Coronation funds sits in the top quartile over five years to May 2026. Their Balanced Plus Fund — their flagship, and a cornerstone of more South African retirement portfolios than any other single strategy — has had a difficult run. Their overweight to domestic assets during a period of SA underperformance, several costly macro calls, and the natural headwind of managing more than R300 billion in assets have all contributed. Managing money at Coronation’s scale is genuinely hard: liquidity constraints limit what can be held, and the funds become increasingly correlated with the benchmarks they’re supposed to beat.

This is not a write-off of Coronation as a manager. Their seven-year numbers are better, and their research capability remains deep. But the five-year picture reflects a real performance gap that the industry has largely acknowledged, and it would be dishonest not to name it.

Ninety One: Growth in Retreat

Ninety One emerged from Investec as an independent business in 2020 with a strong brand, excellent institutional relationships, and a quality-growth investment philosophy. That philosophy was well suited to the 2010s. The 2021-to-2026 period — marked by inflation, interest rate normalisation, and a significant rotation from growth to value — was more challenging. Two of thirteen qualifying Ninety One funds sit in the top quartile over five years. Their Opportunity Fund and Global Franchise Fund, both prominent strategies, have lagged their respective peer medians over the period. Like Coronation, Ninety One remains a capable manager with a clear investment philosophy. That philosophy simply hasn’t been rewarded in the five-year window our analysis captures.

The Boutiques Worth Watching

Three managers sit just outside our top five and deserve specific mention.

Granate Asset Management would rank second in our composite on a pure-numbers basis — 100% of their qualifying funds land in the top quartile, with two of three reaching the top decile. Their Balanced Fund at 16.0% and Flexible Fund at 16.1% are genuinely elite results in large peer groups. The reason we don’t include them in the top five is transparency, not performance: their qualifying range is limited to three funds, and limited seven-year track record data means we can’t apply our confirmation filter with confidence. This is a boutique to follow closely. If the next two to three years maintain what they’ve built, their claim on a top-five spot becomes very difficult to dispute.

Camissa Asset Management — the rebranded Kagiso Asset Management — sits at eleven in our full ranking, but with a noteworthy feature: four of four top-quartile funds over five years also confirm on seven years. That perfect confirmation rate, across equity, medium equity, and income, reflects a genuine and durable process. Their Equity Alpha Fund and Stable Fund are particularly strong. Camissa is a manager whose results are starting to get the recognition they’ve quietly been earning for some time.

ABAX Investments continues to produce exceptional results in their core mandates — their Balanced Fund returned 15.4% over five years, placing it in the top decile of a 189-fund category. The Amplify SCI Flexible Equity Fund, which ABAX sub-advises, similarly sits in the top decile. The challenge for ABAX in our composite is that a small number of their global mandates pull down their overall hit rate. When they’re firing, they’re genuinely elite — the consistency of that elite performance across their full range is what the composite is designed to stress-test.

A Word on Passive Investing

We run this analysis focused on active management because that is where most of the debate, and most of the fee spending, sits. But it would be misleading not to acknowledge what the passive data shows. Satrix, the primary index-tracking provider in South Africa, would rank fourth in our composite if included alongside active managers — ahead of Fairtree, M&G, and most of the market.

Their Balanced Index Fund at 13.4% over five years is top decile in a 189-fund category. Their Low Equity Balanced Index at 11.4% is similarly top decile. The MSCI World Index Fund at 14.9% is top quartile globally. All three confirm on the seven-year horizon. At fees typically well below 0.5% per annum, those returns are even more meaningful in the hands of the end investor.

This is not an argument that everyone should index everything. There are active managers — several of them above — who have genuinely added value and whose process gives reasonable grounds to expect they will continue to. But any honest assessment of the asset management landscape in South Africa has to acknowledge that passive investing is no longer the consolation prize it was once positioned as. It competes directly and successfully with the majority of active strategies across most asset classes.

What This Means for Portfolio Construction

Our rankings are a starting point, not a finish line. Identifying strong managers is the beginning of the conversation, not the conclusion of it. The next step — the one that actually determines outcomes for clients — is understanding how different managers complement one another within a portfolio, and whether a particular manager’s style is appropriate for a specific client’s timeline, income needs, and risk appetite.

A client drawing down in retirement has different requirements from one still accumulating. A retiree in a living annuity needs income stability and downside protection alongside growth; an aggressive accumulator has more tolerance for the short-term volatility that comes with concentrated, high-conviction strategies. For more on how we think about this, our retirement planning guide is a good starting point.

Rankings also change. The managers at the top of this year’s list may not be there in three years. What we are trying to surface is not a static “buy” list, but a picture of where consistent investment skill has shown up — across broad peer groups, over meaningful time periods, confirmed by longer track records. That picture changes slowly, not annually. The fact that Allan Gray has moved from the shadows back to the top of the table, or that Coronation has moved in the other direction, reflects meaningful shifts in performance that accumulated over time.

At Henceforward, our portfolios draw from across this universe — blending managers where the evidence supports it, and being willing to move away from household names when the data no longer justifies their inclusion. That is what fee-only, independent advice should look like.

Do also read our ‘love letter’ to the asset management industry and some of the things that really frustrate us based on what we keep on seeing and hearing.

Frequently Asked Questions

Who are the best asset managers in South Africa in 2026?

Based on our composite scoring across five-year performance data to end May 2026, our top five active asset managers are Allan Gray, PSG Asset Management, Truffle Asset Management, Fairtree Capital, and M&G Investments. The ranking uses a tiered hit rate (top decile weighted 3x), breadth across ASISA categories, a difficulty weighting for peer group size, and a seven-year confirmation filter.

Why is Allan Gray ranked number one in 2026?

Allan Gray tops the ranking on the strength of top-decile performance across four ASISA categories, with four of five top-quartile funds confirmed over the seven-year track record. This combination of breadth, quality, and durability — across market cycles, not just one favourable window — is what puts them at the top. Their value-oriented process underperformed for an extended period and has now been meaningfully vindicated by five years of data.

Why did Fairtree drop from number one to number four?

Fairtree remains a high-quality manager and their drop from first is narrow and specific: their flagship Balanced Fund returned 12.2% p.a. over five years, 11 basis points below the top-quartile cutoff in a 189-fund category. That same fund confirms top quartile over seven years. The rest of Fairtree's range — equity, global equity, income, fixed income — continues to perform strongly. The ranking reflects a tight five-year window on one key fund, not a deterioration in quality.

What happened to Coronation and Ninety One?

Both managers have had a difficult five-year period relative to their peer groups. Coronation placed 1 of 11 qualifying funds in the top quartile over five years; Ninety One placed 2 of 13. This reflects style headwinds, scale constraints, and in Coronation's case some costly macro positioning. Neither is a write-off — both retain capable research teams and longer track records that remain credible. But the current five-year picture reflects a genuine performance gap that advisers and investors should be aware of.

Is Truffle Asset Management worth considering?

Truffle has one of the strongest consistency records of any South African manager. Every fund that qualified in the top quartile over five years also confirms over seven years — a perfect confirmation rate. They sub-advise mandates under the Amplify and Nedgroup brands, so their reach is broader than their own label suggests. For investors looking for focused, durable performance rather than a large product range, Truffle belongs in the conversation.

Final Thoughts

The story this year’s data tells is not a simple one. It is not “value is back and growth is dead” — it is more nuanced than that. What it does suggest is that investment processes built on discipline, patience, and genuine conviction tend to produce results that survive scrutiny over time. Allan Gray waited. PSG waited. Truffle never deviated. All three are at the top of this ranking as a result.

It also suggests that brand recognition is a poor proxy for current performance. Coronation and Ninety One are serious organisations with serious people. Their current rankings reflect a period — not a permanent verdict. Equally, names like M&G and Granate that most investors don’t associate with “top manager” are producing data that demands attention.

The methodology we use will continue to evolve. Rankings are a tool, not a gospel. What they are useful for is identifying where consistent skill is showing up — and prompting the right questions when a familiar name is no longer justifying its position. Both of those things matter, particularly for investors approaching or navigating retirement, where manager selection compounds over time in ways that matter to real outcomes.

If you’d like to understand how your current fund selection and portfolio construction holds up against this landscape, we’re happy to take a look.

Now Read: The Best Performing Balanced Funds to Consider for Your Retirement Annuit

Related: Offshore Investing in South Africa: A Practical Guide

Wondering how your current fund lineup stacks up against this landscape — and whether the managers you hold still earn their place? We review fund selection and portfolio construction against the data, independent of any product or platform. It’s a practical conversation, not a sales pitch.

This article is for general informational purposes only and does not constitute financial, investment, tax, or legal advice, nor a recommendation, endorsement, or criticism of any asset manager, fund, or product named. Henceforward (Pty) Limited is an authorised representative of Graviton Wealth Management (FSP 8772).

The rankings reflect a specific, proprietary methodology applied to third-party performance data (sourced from Morningstar) as at 31 May 2026. While this data is believed to be reliable, Henceforward does not warrant its accuracy or completeness, and figures may be subject to revision or restatement by the underlying providers. Different methodologies, periods, or data sources may produce materially different results.

Past performance is not a reliable indicator of future results. Manager and fund names are the property of their respective owners. Any errors or omissions are unintentional and excepted (E&OE). Consult a qualified financial advisor before making any investment decisions.

Carl-Peter has been in the financial services industry since 2003 and launched Henceforward with Steven Hall in 2021. He focuses primarily on investment strategy and portfolio construction. Henceforward is a fee-only, flat-fee firm — no commissions, no product incentives.